The Economics of Stability

In our first post, we introduced ParityUSD, an innovative over-collateralized stablecoin on Bitcoin Cash (BCH). Today, we’ll dive deeper into what makes ParityUSD stable.

Unlike trusted stablecoins which rely on centralized custodians and use traditional banks to hold dollars for backing, decentralized stablecoins use economic mechanisms to stabilize their price at $1. The big advantage of decentralized is that they remove the trust required for middlemen and create a neutral, transparent system.

In this blogpost we’ll explore how ParityUSD is over-collateralized by Bitcoin Cash as backing asset and how the stability mechanisms ensure the stablecoin maintains its 1:1 peg to the US Dollar, even in volatile market conditions.

Redemption Mechanism

At the heart of ParityUSD’s stability is its redemption mechanism: at any point you can redeem 1 PUSD for $1 worth of Bitcoin Cash. Conceptually this answers the question of “why would the token be worth 1 dollar?“.

A redemption mechanism is also what’s used for centralized stablecoins: they can usually be redeemed directly for dollars from the backing bank account.

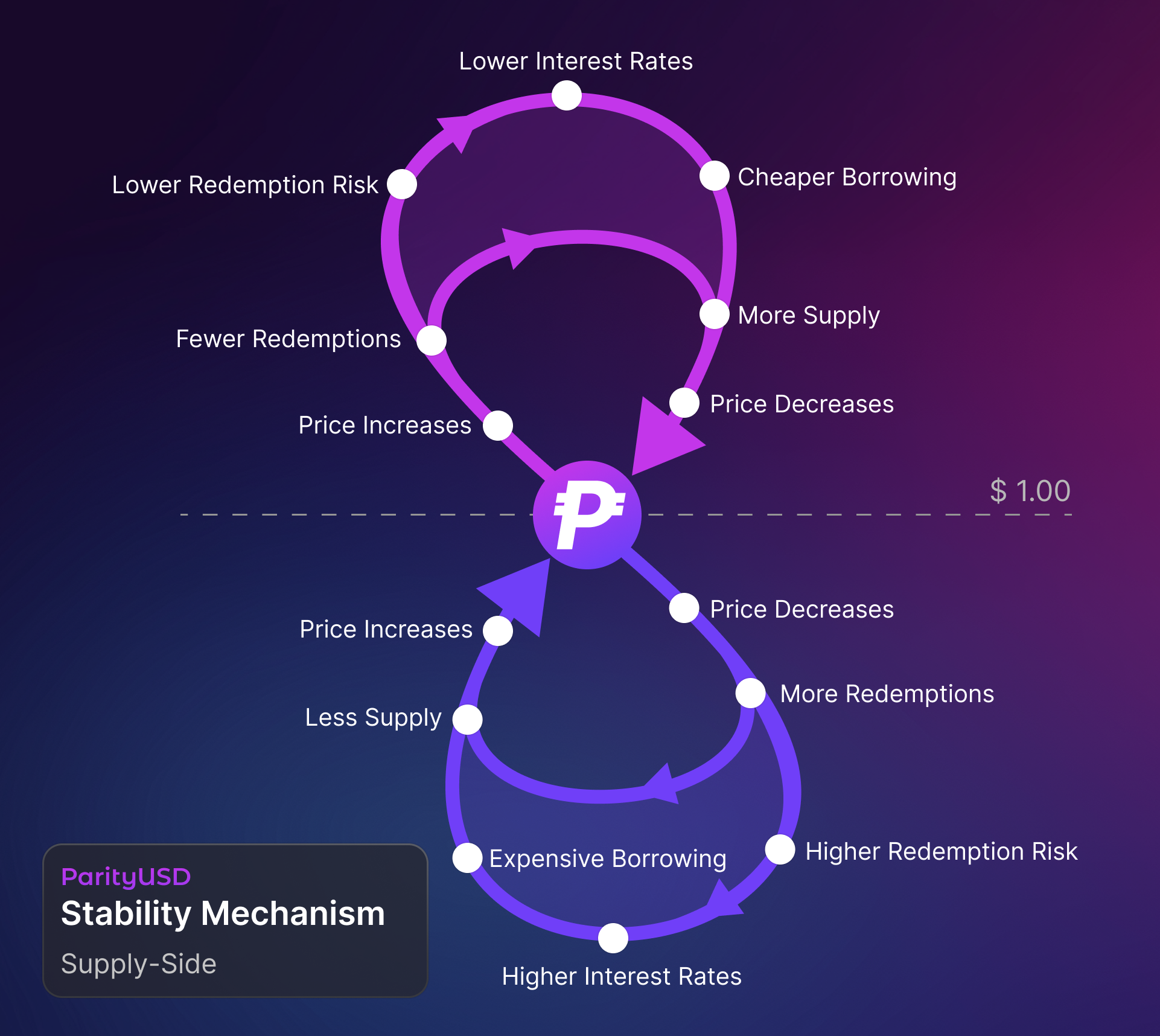

The redemption mechanism creates a direct arbitrage opportunity: if ParityUSD’s price drops below $1, users can purchase ParityUSD at a discount and redeem it for $1 worth of Bitcoin Cash. This arbitrage drives the price back to the lower bound of $1.

From the stablecoin holder’s perspective this redemption mechanism is a great assurance! However, from the borrower’s perspective - who created an over-collateralized BCH loan - being redeemed against presents a new risk, because they essentially allow others to convert their BCH collateral to stablecoins. We’ll expand on how borrowers are affected by redemptions in the next section.

Market-driven Interest Rates

In 0% interest-rate systems like Liquity v1, the redemption mechanism is tied to the loan’s collateral ratio where the loans with the lowest collateral ratio are redeemed against first. This caused large inefficiencies during periods when there’s downward pressure on the $1 peg as this creates frequent redemptions, which in turn leads to the need for very high collateral ratios. To address these issues, ParityUSD adopts the market-driven interest rate mechanism from Liquity V2.

In the Liquity V2 design, each loan can set its own interest rate. The redemption mechanism then works by redeeming against the lowest interest-paying loan first. Because interest rates are user-set, active loans will use a range of different rates, but this range is market driven: when redemptions occur, borrowers may want to adjust their interest rates to avoid having their loans redeemed. Conversely when almost no redemptions occur, borrowers may want to lower their interest rate to reflect this low risk. By pricing redemption risk separately from collateral ratio, the system redeems first against the borrower who values not-being-redeemed-against the least.

The going (average) interest rate in the system influences the supply of ParityUSD: higher rates make borrowing more expensive, reducing the incentive to mint new ParityUSD and tightening supply. Market-driven interest rates tied to redemption risk naturally counterbalances price deviations of ParityUSD, as illustrated in the following graphic:

The interest rate paid by borrowers also has a demand-side effect; we will later extend this graphic to include this effect.

Delegating Interest Management

In the Liquity V2 design borrowers can choose to manage their interest rates manually or delegate this task to an automated interest rate manager. ParityUSD will adopt this crucial aspect to create a responsive and dynamic interest rate.

Users who prefer self-management can set and adjust their interest rates manually, responding directly to market conditions. Alternatively, borrowers can delegate this task to an interest rate manager, which continuously monitors market conditions and adjusts rates according to the borrower’s risk profile. For example, when demand for ParityUSD is high and redemption risk is low, the manager might lower rates to encourage borrowing and increase supply. Conversely, when redemption risk rises, the manager can raise rates to discourage borrowing and protect against redemptions.

Delegating interest management does not give any control over the loan’s collateral to the interest manager, it just allows the manager to update the loan’s interest rate. Moreover, this authorization can easily be “revoked” and switched back to manual management, or to a different interest manager. This flexible approach, combining manual and automated options, allows for a dynamic and adaptable interest-rates for loans.

The Stability Pool

The Stability Pool is a crucial element in ParityUSD’s stability system. The stability pool manages the ParityUSD deposited by users who wish to stake their stablecoins to earn yield. The Stability Pool receives the BCH interest paid by borrowers and pays this out as yield to the stakers in the stability pool.

Secondly the Stability Pool functions as the liquidator: when a borrower’s loan becomes under-collateralized, the instant liquidation mechanism is triggered. In this process, a portion of the staked ParityUSD is converted into Bitcoin Cash (BCH) at a discount, which is then distributed to the stakers. This means that staking in the Stability Pool is not without risk: users willing to stake must be prepared for their staked ParityUSD to be converted into BCH during liquidations, which can result in gains or losses depending on market conditions.

The exact percentage yield (APY) cannot be predicted in advance, as it varies based on the demand and supply of ParityUSD, the number of stakers, and the occurrence of liquidations. The fewer ParityUSD is staked in the liquidator, the higher the yield for individual stakers, as they receive a larger share of the total interest paid by borrowers. This creates an arbitrage mechanism where individuals may borrow ParityUSD specifically to stake it in the pool when there are few stakers. This behavior ensures strong incentives for staking, particularly when the pool has limited funds to process liquidations, keeping the Stability Pool well-funded and effective in its ability to liquidate bad loans.

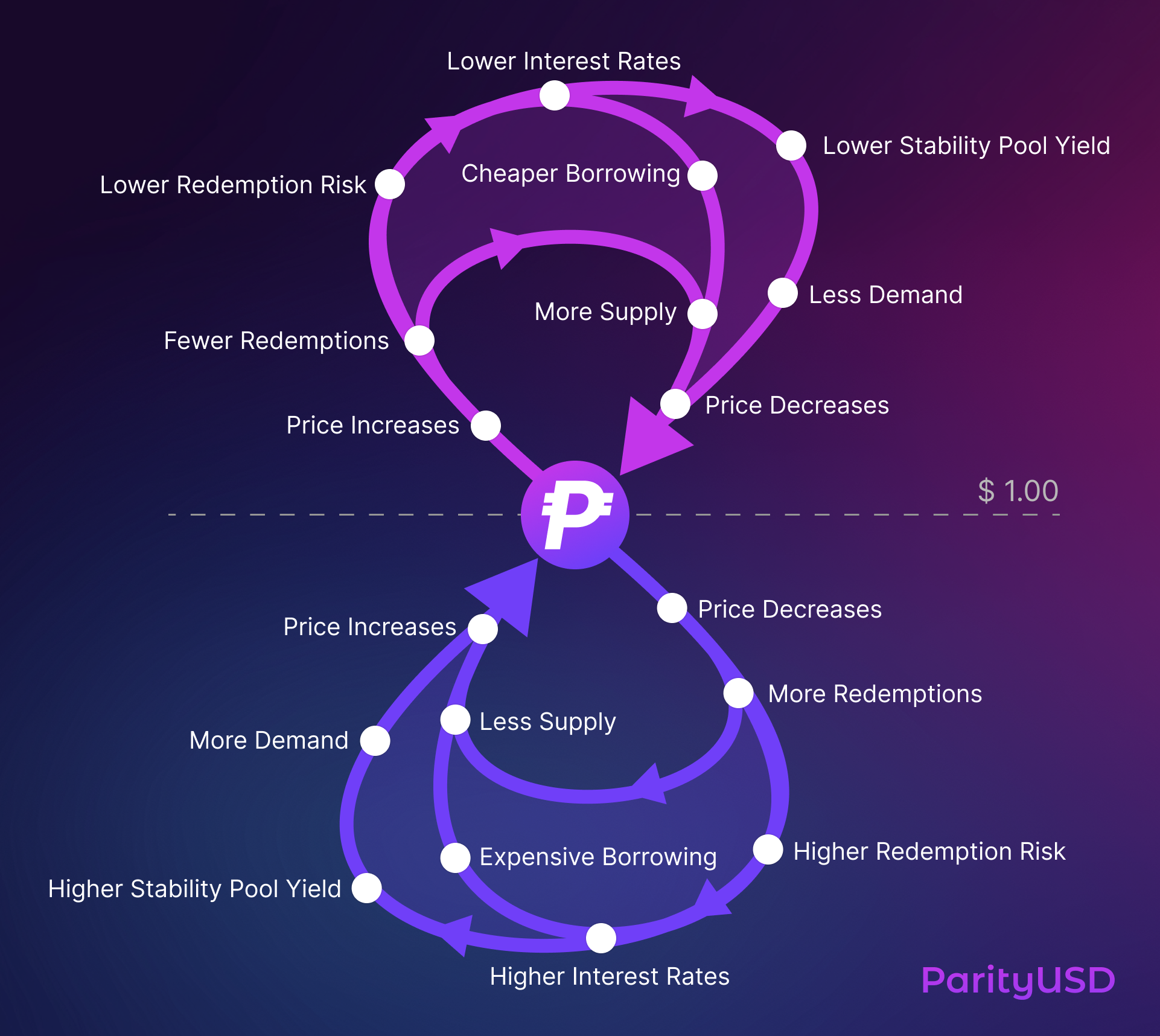

Because the stakers earn the interest rate payments as yield, the going rate affects the demand for ParityUSD: higher rates boost the yield for Stability Pool stakers, increasing demand as users seek to earn this yield. Conversely, when interest rates drop, borrowing becomes more attractive, increasing supply, while lower yields would reduce this demand. We expand the previous graphic with this additional mechanism:

Through these interconnected mechanisms, ParityUSD has a very strong schelling point to self-correct to the $1 price-point, balancing supply and demand with emergent user-controlled, market-driven adjustments.

Sustainable Real Yield

The yield offered by ParityUSD is both sustainable and real, paid directly by borrowers in BCH through interest payments and liquidation fees, rather than being speculative or inflationary. This yield is crucial for balancing the system by incentivizing a well-funded Stability Pool for liquidations and boosting demand for ParityUSD. When the stablecoin trades below $1, redemptions increase, raising interest rates and the corresponding yield. This higher yield increases demand by encouraging users to stake their stablecoins and it reduces the circulating supply by making borrowing more expensive, and this way it drives the price back to the $1 equilibrium.

Market conditions, reflected through dynamic interest rates, determine the APY that stakers earn. When redemptions are high or there are fewer stakers, the yield increases, attracting more capital to the Stability Pool. Conversely, when there are fewer redemptions or more stakers, the yield decreases.

By enabling stakers to earn yield, ParityUSD creates continuous demand and liquidity within the ecosystem. This not only strengthens the stability of the stablecoin but also enables its role as a dollar-savings account on Bitcoin Cash. This makes it a valuable financial tool within the Bitcoin Cash network, to draw in new users and capital into the BCH DeFi ecosystem.

Balancing Supply and Demand

ParityUSD balances supply and demand through an integrated system of redemptions, dynamic interest rates, and the Stability Pool. Unlike governance-driven systems like DAI (now USDS), where interest rates can change arbitrarily and abruptly, or algorithmic models that can cause volatile swings or be badly parameterized, ParityUSD’s market-based interest rates are neutral, adaptive and dynamic. This ensures that going interest rate is not arbitrary but instead accurately reflects market conditions: global interest rates, DeFi interest rates and BCH-specific variables. Interest rates are perhaps the most important economic price signals of all, so from a free-market perspective it’s clear these should not be centrally-planned. Instead interest rates - like other important price signals which enable efficient allocation - should be an emergent market phenomenon.

As shown in the graphic, redemptions have first-order and second-order effects. The immediate goal of redemptions to create a hard lower-bound by enabling direct arbitrage. Secondly redemptions are driver behind the interest rate mechanism which in turn regulates the cost to borrow and the rewards for stakers. By using market-driven interest rates, the system is “efficient” in that it redeems the borrower with the least redemption-aversion first. Then because of increased redemption risk the price signal of the going interest rate communicates to other borrowers that they have to decide if it makes sense to pay a higher interest or accept higher redemption risk. This way the system continuously answers the questions “what should the going interest be for borrowing to not be redeemed against”, “what should the going APY be for staking” and ultimately “how much ParityUSD should be in circulation?“.

Each user in the ParityUSD system manages their own loan based on market redemption risk. If interest rates rise due to increased redemptions, users can choose to repay their loans. Even when redemptions occur, borrowers do not lose all their BCH — as redemptions pay back part of the loan debt but take out a corresponding amount of BCH - so the excess collateral remains in the borrower’s possession even when the full loan got redeemed.

Conclusion

The Bitcoin Cash ecosystem has long needed a decentralized, trust-minimized stablecoin, and ParityUSD is designed to fill that gap. By integrating redemptions, dynamic interest rates, the Stability Pool, and sustainable yield, ParityUSD has a robust stability mechanism that maintains a tight peg to the US Dollar. This innovation empowers BCH holders by providing stability, borrowing, and staking opportunities, addressing key needs within the BCH DeFi landscape.

ParityUSD leverages Bitcoin Cash’s unique strengths—scalability and low transaction fees. These features make BCH an ideal platform for a decentralized stablecoin, allowing ParityUSD to operate efficiently and scale effectively. As the BCH network continues to evolve, ParityUSD is poised to drive significant growth in the stablecoin market, catalyzing the expansion of decentralized finance on Bitcoin Cash.

Join the Conversation

Stay informed about our progress and dive deeper into the details of the ParityUSD project by following our updates. We invite you to be part of the discussion and join the community.

- Follow ParityUSD on X: x.com/ParityUSD

- Join the ParityUSD group on Telegram: t.me/parityUSD

In our Telegram group, you’ll have the opportunity to engage directly with the team and developers—ask questions, share your thoughts, and be part of the ongoing conversation as we build ParityUSD together!